The European Parliament on 16 April 2019 has adopted a new, comprehensive regulatory regime for investment firms: the Investment Firm Directive (“IFD“) and Investment Firm Regulation (“IFR“) are intended to replace the existing applicable regulation for investment firms.

While small and “non-interconnected” firms in particular will benefit from less regulation, the legislation for “systemically relevant” investment firms means no less than equal treatment with credit institutions in the sense of a level playing field – accordingly, they will fall entirely under the previous regulatory framework (i.e. Capital Requirements Regulation 575/2013 (“CRR”)). As a result, all other investment firms will no longer be subject to the CRD/CRR framework, which is primarily intended for banks.

The final vote of the European Parliament on the legislation took place in mid-April 2019. Moreover, on 5 December 2019 both the regulation and directive have been published in the official journal of the European Union. The new rules, IFR and IFD, have to be transposed into national law by the end of 2020 and early 2021 respectively.

A transition period of five years for capital requirements, during which capital requirements will be limited to twice the firms’ current capital requirements under CRR (or twice their fixed overheads in the case of firms which were not subject to capital requirements under CRR) will apply. Also, CRR market risk rules will continue to apply for five years or until the application of CRR 2 (Regulation (EU) 2019/876) market risk rules, whichever is later.

Scope of Application

The new regulatory regime applies to ALL investment firms authorised and supervised under the MiFID II (European Directive 2014/65/EU).

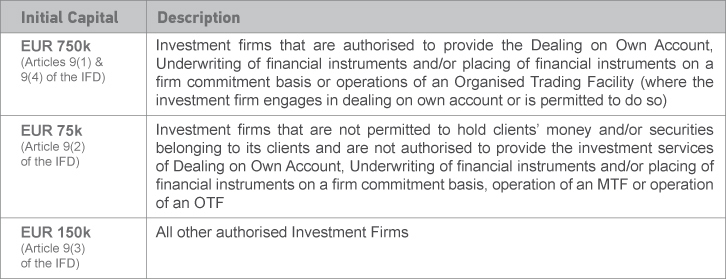

New Initial Capital Requirements and Revised Classification

The new regime revises the Initial Capital Requirements for investment firms. Specifically, the Initial Capital for investment firms is illustrated in the Table 1 below:

Table 1

Existing Investment Firms will be required to maintain own funds of at least the new initial capital limits mentioned above.

The following composition of capital should be eligible for meeting the capital requirements (pursuant to Article 9 of the IFR):

- CET 1 capital should constitute at least 56% of capital requirements;

- Tier 1 capital should constitute at least 75% of capital requirements;

- Tier 1 and Tier 2 capital should constitute at least 100% of capital requirements

CET1, Tier 1 and Tier 2 are calculated in accordance with the eligibility criteria of the capital instruments as per the provisions of the CRR.

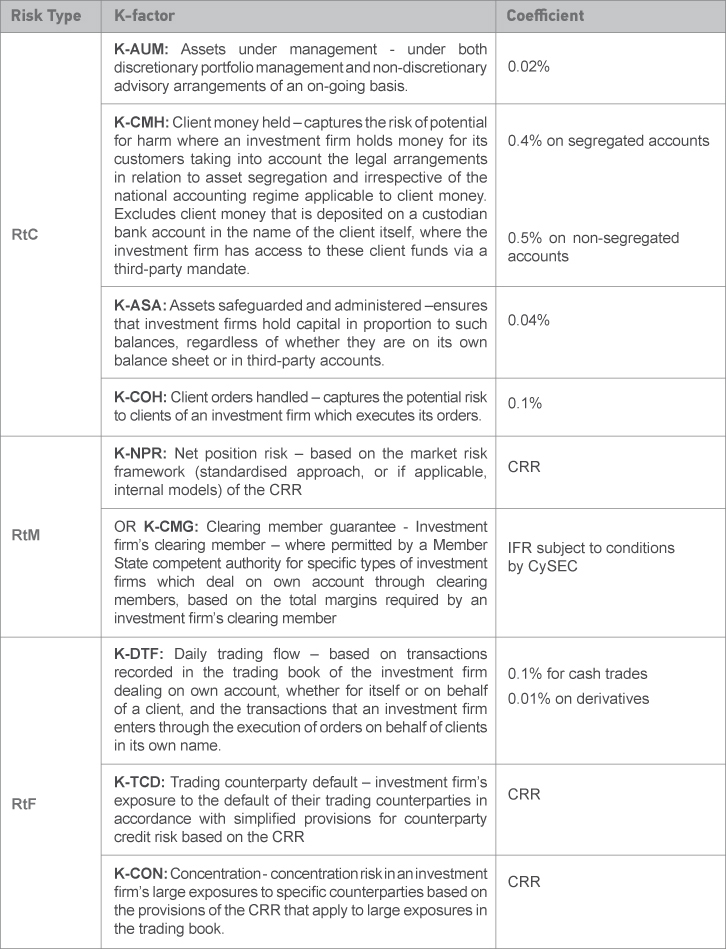

New Pillar I Framework: K-Factors Methodology

Capital requirement from applying K-factors formula (pursuant to Article 15 of the IFR) is the sum of Risk to Customer (‘RtC’), Risk to Market (‘RtM’) and Risk to Firm (‘RtF’). Moreover, in order to calculate these factors, investment firms are required to multiply the metrics indicated in the Table 2 below, with the respective coefficient.

Table 2

The proposal introduces a new categorisation of investment firms in order to ensure that prudential requirements are tailored to the size, nature and complexity, as shown in the Table 3 below.

Table 3

Large exposures

Investment firms under class 2 and class 3 (subject to exemptions) shall monitor and control their large exposures so as not to exceed the following limits (per Article 37 of IFR):

- An investment firm’s limit of an exposure value with regard to an individual client or group of connected clients shall be 25% of its own funds.

- Where that individual client is a credit institution or an investment firm, or where a group of connected clients includes one or more credit institutions or investment firms, the limit of the exposure shall be the higher of 25% of the investment firm’s own funds or EUR 150 million provided that for the sum of exposure values with regard to all connected clients that are not credit institutions or investment firms, the limit remains at 25% of the investment firms’ own funds. Where the amount of EUR 150 million is higher than 25% of the investment firm’s own funds, the limit of the exposure shall not exceed 100% of the investment firm’s own funds.

Liquidity Requirement

Under the new prudential regime, investment firms under class 2 and class 3 shall hold an amount of liquid assets equivalent to at least one third (1/3) of the fixed overheads requirement. The IFR specifies the instruments that are eligible to be classified as liquid assets to be included in the calculation of the said ratio. Moreover, competent authorities may exempt from the liquidity requirement investment firms that meet the conditions for qualifying as small and non-interconnected investment firms.

Disclosure Requirements

The IFR/IFD set a wide range of disclosure obligations for Class 2 investment firms (and to any class 3 firms that issue additional tier 1 capital instruments). Specifically, public disclosures are required in respect of:

- Risk management objectives and policies

- Internal governance arrangements

- Own funds requirements

- Remuneration policy and practises

- Investment Policy

- Environmental, social and governance risk

Reporting Requirements

Pursuant to article 54 of the IFR, class 2 investment firms shall report to their Member State competent authority, on a quarterly basis, the following items:

- Level and composition of own funds

- Own funds requirements and calculations

- Where the firm is a class 3 firm – the level of activity, including the balance sheet and revenue breakdown by investment service and applicable K-factor.

- Large exposures

- Liquidity requirements.

Class 3 investment firms are required to submit the above on an annual basis.

The details of the prudential requirements for each class is presented in the Table 4 below

Table 4

Other supervisory measures

The IFD requests the investment firms under class 2 to have in place sound, effective and comprehensive arrangements, strategies and processes to assess and maintain on an on-going basis the internal capital and liquid assets that they consider adequate to cover the nature and level of risks which they may pose to others and to which the investment firms themselves are or might be exposed (ICAAP). This process needs to be appropriate and proportionate to the nature, scale and complexity of its activities.

The class 3 investment firms may also be requested to the ICAAP requirements to the extent they deem it to be appropriate.

Prudential consolidation

Investment firm groups should examine the criteria set in Article 46 of IFD in order to determine whether they fall under consolidated supervision. The prudential consolidation requirements are set out in Article 7 of IFR.

Our team of high calibre professionals with years of experience in the financial services industry stands ready to assist in the following ways:

- Analysis and impact of the new prudential regime on your Company

- Consultation regarding IFR/IFD enquiries

- Monitoring of the Company’s capital adequacy based on the new prudential framework

- Revision of the Company’s risk management related policies

- Assistance with the capital adequacy reporting obligations and compliance with the new requirements.

For more information, please feel free to contact our Risk Management Experts here.